Quarantine is quarantine, but reporting has not been canceled, therefore the seminar on TP conducted by Larysa Vrublevska, Auditor, Partner, Head of Transfer Pricing Practices of the EUCON Legal Group, on June 19, became especially relevant.

The online event was organized by the Federation of Professional Accountants and Auditors of Ukraine and the Association of Taxpayers of Ukraine.

Larysa Vrublevska within the topic “Peculiarities of reporting on TP for 2020″started the seminar on new changes to the Tax Code of Ukraine (Law changes 466-ІХ), aspects of reporting in the field of transfer pricing for 2019, information on controlled transactions. In addition, the expert considered self-adjustment of the price of the controlled transaction and the amount of tax liabilities of the taxpayer, corrections to the report on controlled transactions and to the Declaration of income tax, list of controlled transactions 2019, cost criterion, business transactions between a non-resident and its permanent establishment in Ukraine. The issues of calculating the volume of transactions with the counterparty, the cost criterion and the amount of annual income were supported by practical examples and deserved special attention.

Ms. Vrublevska did not miss aspects of the procedure for applying the List 480 in 2019, dividends, assignment of the right of claim, free transfer of goods, non-refundable financial assistance, contribution of authorized capital, purchase of fixed assets to non-residents, also sale of goods through a non-resident commissioner and credit note.

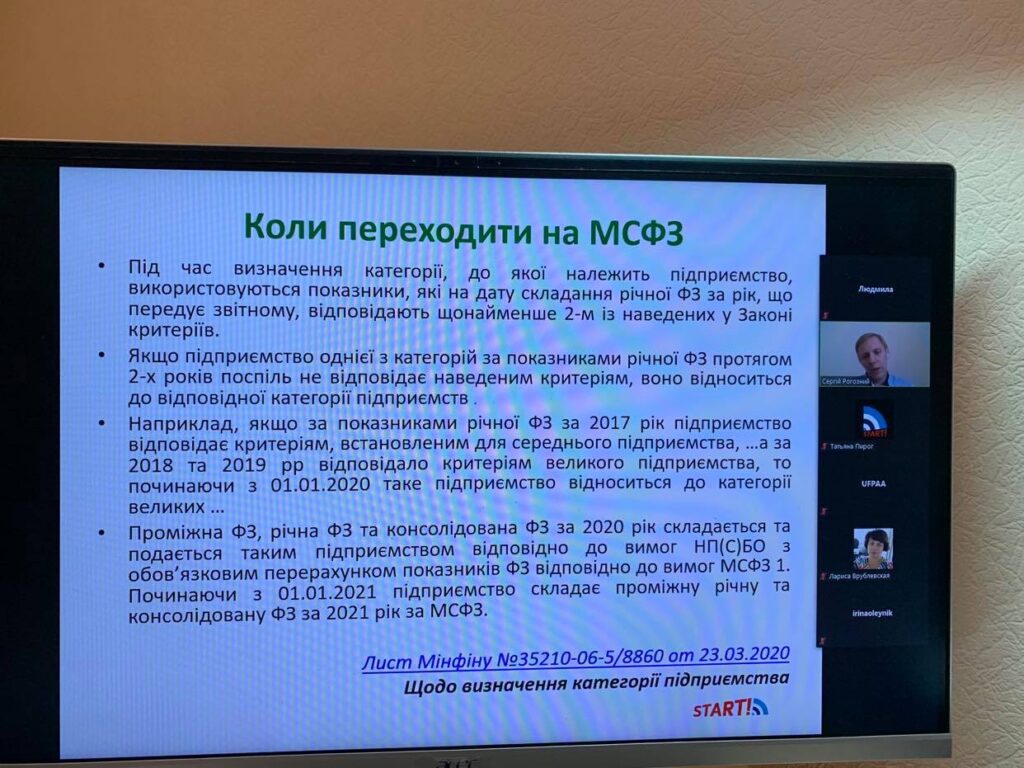

During the seminar the speaker focused in detail on the features of the preparation of transfer pricing documentation, in particular, the need for segmentation of financial statements, the principle of grouping operations, on aspects of control in the field of transfer pricing, ways of monitoring and inspections. The speaker showed the participants examples of practical cases, which successfully reinforced the theoretical basis of the TP reporting process.